One of the first things which the new government announced, to the surprise of nobody, was that the previously announced reforms of the care system would not be going ahead. The reforms, which included a cap on care costs, had already been delayed by the previous government. The withdrawal of the reforms leaves many people in a position where they will have to fend for themselves.

One of our favourite groups of number crunchers, the Institute for Fiscal Studies, has been looking at the care system and its costs, in its report “Adult social care in England: what next?” https://ifs.org.uk/publications/adult-social-care-england-what-next

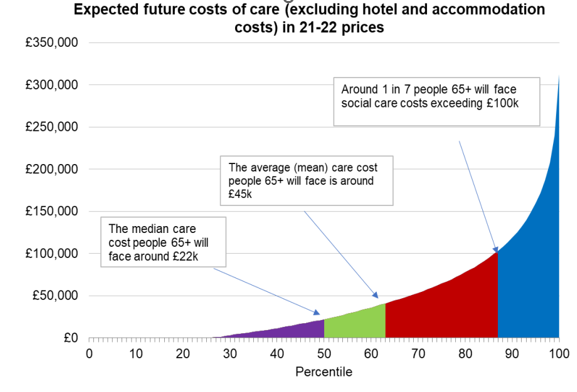

There were a few interesting, new observations in its report.

In order to obtain assistance with the cost of care, it is necessary not only to have a means test (and the thresholds for wealth and income are pretty tight) but also a needs test. The number of older people receiving state-funded care in England has dropped by 10% since 2014 – 15 due to tightening eligibility criteria. For the needs test, local authorities assess individuals’ care needs against national eligibility criteria, but the local authorities set their own assessment procedures. The IFS conclude that the stringency of the needs test also increased over the first half of the 2010s, as councils responded to funding cuts by restricting support to those with the highest assessed needs (House of Commons, 2017). There is also evidence to suggest that councils interpret and implement these criteria differently (Ogden and Phillips, 2023). In 2022–23, for example, just under half (48%) of individuals aged 65 and over who requested support received some sort of short-term or long-term care from their council. But in one-in-ten local authorities, fewer than a third of those requesting support ended up receiving some, while another one-in-ten local authorities provided support to more than 70% of those requesting it (NHS England, 2023a). Considerable local discretion remains, therefore.

The population at older ages in England has grown substantially since 2010 and is projected to continue to grow between now and 2030. Between 2010 and 2024, the English population aged between 65 and 74 grew by 23.2%, the population aged between 75 and 84 grew by 36.8%, and the population aged 85 and over grew by 27.3%. The equivalent figure for the overall population is 10.7%. Between 2024 and 2030, these older groups are again projected to grow more quickly than the population at large, with the greatest proportional increase (17.7%) in the population aged 85 and over – the group that makes heaviest use of adult social care services.

Sadly, the government and local authorities don’t have a magic money tree, so it seems unlikely that more financial help is round the corner. It seems likely that more local authorities will use a stricter interpretation of the needs test in order to keep their budgets under control.

This makes the current situation even worse, where people face the risk of unpredictable and unlimited social care costs – one in seven individuals over 65 will face care costs above £100,000 and roughly one in ten individuals will face care costs above £120,000 over their lifetime. (05.01.2022 Department of Health Adult-social-care-charging-reform-impact-assessment)

So, what can you do to make the best of this bad situation?

Planning ahead is clearly the best approach. Keeping abreast of the likely cost of care, and the chances of having to pay for it, is one requirement. The next is to identify how you will pay for care, if needs be – which of your assets are the best to use to pay for care (this will probably change as tax rules and investments change). Deciding what sort of care you would like (at home or in a home, and the quality of care) is an important choice. And finally, you should ensure that you have the administrative requirements, including powers of attorney in place to ensure that the care fees can be paid. Of course, you must have communicated all of this to the relevant people. Faced with this amount of complex decision making, particularly at a when financial numeracy is declining, many people choose to get professional assistance and advice. We have helped many of our clients plan for their potential care needs and to implement their plans, if and when the time comes.

Philip Wise | philip@sussexretirement.co.uk

Managing Director and Chartered Financial Planner

This blog is for information purposes and does not constitute financial advice, which should be based on your individual circumstances.